The UK is facing a “double whammy” as higher-for-longer interest rates begin to bite, with the country particularly vulnerable to a pullback in consumer spending and knock on consequences for corporate debt.

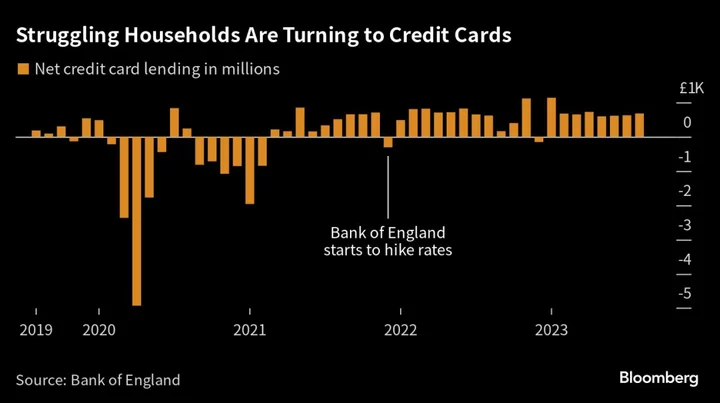

The Bank of England warned this week that the full impact of elevated borrowing costs has yet to fully pass through, although about two thirds of UK adults have already cut back on discretionary purchases and retail sales are almost flat by volume. More households are also turning to credit card debt, which is growing by double digits annually.

The country’s weak level of investment puts more weight on consumer spending, said John Van Reenen, a professor at the London School of Economics.

“This becomes a ‘doubly whammy’” because “UK rates have risen more sharply and because Britain relies more on consumption,” Van Reenen adds. “These heavy chains are pulling down our growth prospects.”

Strong growth would help firms grappling with higher borrowing costs to boost revenue and service their debt. Instead, the metric remained weak in August and the outlook is expected to remain stagnant, with the IMF slashing its forecast for next year from 1% to 0.6% this week. A consensus estimate compiled by Bloomberg is even lower at 0.4%.

More than $15 billion of UK corporate debt is trading at distressed prices, according to data compiled by Bloomberg News — up nearly 50% since late last month.

One in two companies is likely to face stress in servicing their debt by the end of the year, the Bank of England has warned, which could cause some owners to cut investment and employment sharply.

The reliance on consumer spending also filters into the debt markets. About 35% of high yield bonds and leveraged loans issued by UK firms are in the consumer discretionary sectors, according to data compiled by Bloomberg, making the industry potentially more vulnerable to a recession than the rest of Western Europe where it makes up 26% of the market.

The vulnerability, in turn, harms the attractiveness of UK corporate debt. On top of that, the BOE’s quantitative tightening program, in which it is selling off bonds bought during a decade of almost free money, is causing spreads to narrow, making company bonds issued in sterling less appealing.

Read More: UK Sours on £895 Billion Stimulus Tool as Side Effects Mount

Property Woes

One reason for the weakening consumer is that mortgage payments have soared for homeowners and landlords who are refinancing off historically cheap rates. That’s already starting to affect the market for buy-to-let mortgage debt that was bundled up and sold to investors as bonds.

In the second quarter, “we noted a sharp 60% increase in BTL arrears compared to 12 months prior,” said Cristina Pagani, a director at Fitch Ratings. Although still low in absolute terms, it “could signal the start of performance deterioration in the sector.”

In addition, there may be some weakness in so-called non-conforming mortgages, which are loans to homeowners who don’t meet the typical mortgage criteria from high-street banks.

“We continue to expect an uptick in arrears in securitized pools, particularly in the non-conforming sector, where borrowers on floating rates are facing the burden of higher interest rates,” Pagani said.

Activity in the wider housing market has also slumped, with most indicators deep in negative territory, according to a survey by the Royal Institution of Chartered Surveyors.

In the commercial real estate market, listed REITs could also face higher borrowing rates if the pound weakens and swap rates rise, said Sue Munden, a senior real estate analyst at Bloomberg Intelligence.

Private sector landlords are more vulnerable than their listed counterparts because they took on more leverage and, with prices falling, lenders may demand that they sell assets to recoup their loans.

“Forced private sales could push property prices down further and increase pressure on the higher levered listed companies,” she added.

Brexit Selloff

Rising rates have been hurting private equity firms who went on a shopping spree in the UK from 2017 through 2021, taking advantage of a so-called Brexit discount and cheap borrowings. Household names from Wm Morrisons to John Laing Infrastructure Ltd were bought up and loaded with leveraged debt.

Many buyout firms failed to buy protection against interest rate hikes, meaning the cost of repaying the debt soared. For example, Morrisons was unhedged until at least Sept. 2022, according to Moody’s Investors Service, and though the grocer eventually put hedges in place for a portion of its debt, it was still on the hook for £375 million ($397 million) in interest on a pro-forma basis in its most recent fiscal year.

“The leveraged loan corner of the market is where you see the more vulnerable parts of the economy and that’s where most of the concern is focused,” said Peter Chatwell, head of global macro strategy trading at Mizuho Plc, who was speaking generally about British companies.

Tipping Point

Even beneficiaries of higher rates may soon start to suffer. Financial firms could be near a tipping point “where deposit costs start ramping and credit quality deteriorates,” said Tim Craighead, a senior European equity strategist at Bloomberg Intelligence.

That’s showing in insolvencies, which have been increasing since early 2021, according to data compiled by a government agency, as small businesses default on more loans, a trend that was expected to spread to medium-sized firms in the third quarter.

Shrinking Market

For those companies big enough to do so, raising money in euros and dollars can be more attractive than pounds because policy rates are 125 basis points higher in the UK than in the euro region.

The move away from the UK market can be seen in the leveraged loan market, which saw its first quarter this year without any sterling deals, and in refinancing activity. KKR-backed food group Upfield BV for example recently retired a sterling-denominated facility, replacing it with longer-term euro and dollar loans.

Even in Europe’s publicly-syndicated debt market, the issuance of high-grade debt denominated in pounds from non-financial firms has remained at a trickle for several years, with borrowers instead piling in to the more liquid euro funding market. The sterling corporate bond market has now shrunk in value by about a fifth since the end of 2021, according to one blue-chip debt index.

Hunt for Cash

That’s left some British firms exploring alternatives to deal with their debt stacks. The country’s biggest pub chain Stonegate looked at selling 1,000 pubs and using the proceeds to repay some of its liabilities. After that process failed, it’s now looking to move the hostelries into a new entity and raise debt through that.

Look at a list of companies whose debt is trading at wide discounts to par and you can see just how widespread the suffering has become across the economy. Loans and bonds linked to the likes of the Canary Wharf financial center, travel agency Saga Plc and lender Metro Bank Holdings Plc, which has just announced a capital raise and a haircut for some bondholders, are trading at distressed levels.

“The full impact of higher financing costs has not yet passed through to all corporate borrowers,” the Bank of England warned in its financial stability report this week.

Sam Woodward, a restructuring partner at EY, said Britain’s businesses “are increasingly sensitive to the shifting credit landscape,” with the full effect of high rates and weak consumer demand yet to be seen. He added that while 2023 has been relatively calm so far, “Christmas and early 2024 could be a different story.”

--With assistance from Helene Durand and Hannah Benjamin-Cook.

(Updates with latest GDP reading in fifth paragraph.)

Author: Neil Callanan, Giulia Morpurgo and Abhinav Ramnarayan