Wall Street chiefs seeking to explain recent steep drops in trading revenue have reminded investors how lucrative things were a year ago: Goldman Sachs Group Inc. President John Waldron called 2022 “particularly strong.” Citigroup Inc. boss Jane Fraser said “everything was firing on all cylinders.”

Rarely mentioned is one of the reasons for last year’s boom: a billion-dollar windfall funneled from Russia through former Soviet republics to Wall Street’s currency traders.

As Western companies and international investors rushed to exit Russia amid the Ukraine invasion and the sweeping sanctions that followed, they were desperate to swap their rubles for dollars. For currency traders at firms including Goldman Sachs, Citigroup and JPMorgan Chase & Co., it was easy money: They found a way to scoop up greenbacks at a low price and then sell them to those fleeing clients for a healthy markup without running afoul of sanctions, people with direct knowledge of the transactions said.

To pull it off, the people said, the Wall Street firms turned to an obscure source with which they had rarely traded dollars before: lenders based in countries deemed “friendly” by Russia and not sanctioned by the US, such as Halyk Savings Bank of Kazakhstan JSC and First Heartland Jusan Bank JSC and Kaspi.kz JSC in Kazakhstan and Ameriabank CJSC in Armenia. Those lenders were able to buy dollars directly from Russian banks around that country’s local exchange rate, which at times was far less than what was quoted abroad, the people said.

The transactions helped turn small trading desks into money-minting machines and drove a broader surge in fixed-income trading revenue that was the second-highest in a decade. Goldman Sachs, Citigroup and JPMorgan each made hundreds of millions of dollars from the ruble trade as the war ground on last year, according to the people, who requested anonymity as details are private.

“In war, normally two entities make money,” said Jason Kennedy, chief executive officer of financial-services recruitment firm Kennedy Group. “Arms dealers and banks.”

Ruble traders on Wall Street probably saw their annual bonuses doubled, Kennedy said.

Trades Continues

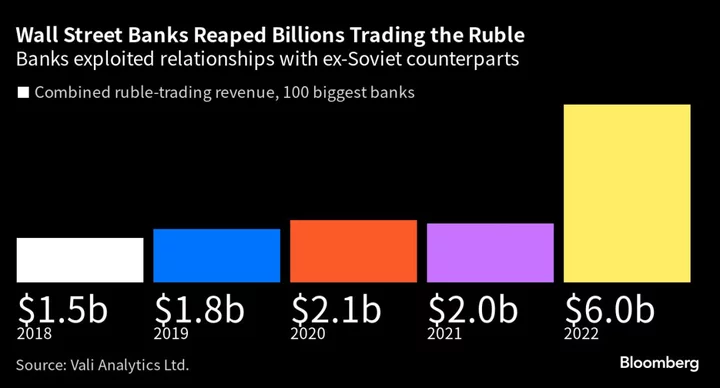

The world’s biggest banks made $6 billion overall last year trading the Russian currency, about triple what they generally make from the business, according to data from Vali Analytics Ltd. Banks continue to trade currencies with Kazakh and Armenian counterparts today, although the deals are less lucrative, the people said.

The Wall Street firms haven’t been accused of any wrongdoing and there’s no suggestion that the trades violated sanctions. Some of the people familiar with the deals said the banks’ trading helped their clients comply with new rules and exit difficult holdings. The US banks already had relationships with the lenders in Kazakhstan and Armenia, the people said.

Still, the two groups hardly ever traded significant volumes of foreign exchange with each other before Russia invaded Ukraine last year, the people said. They quickly became important partners, sometimes trading tens of millions of dollars on a daily basis, the people said.

Wall Street banks have said they benefited from higher activity around clients exiting Russia, but the scale and mechanics of the ruble trade haven’t been previously reported. The profits they made sit next to other deal-making opportunities created by the turmoil of the Ukraine war but also contrast with the costs they took on as they moved staff out of Russia and wound down operations in the country.

Representatives for Goldman Sachs, Citigroup and JPMorgan, all based in New York, declined to comment. Emails requesting comment from Almaty-based Halyk and Jusan weren’t returned. Representatives for Kaspi said the firm hasn’t traded rubles in significant volumes with Wall Street or Russian banks.

Artyom Mkrtchyan, a spokesperson for Ameriabank, declined to elaborate on how much money the Yerevan-based lender had made from the arbitrage but said it was a “modest” share of overall currency transactions.

Some rival Wall Street banks were spooked by the risks and shied from the trade, the people said.

Traders at Bank of America Corp. avoided the arbitrage under broad instruction from Chief Executive Officer Brian Moynihan and his deputies, who told them to avoid any transactions that could lead back to Russia, the people said. Compliance officials at UBS Group AG feared that the deals could be viewed as ducking sanctions and prevented traders at the Swiss lender from pursuing them, according to the people. HSBC Holdings Plc, one of the biggest players in the currency markets, also didn’t take part, one of the people said.

Representatives for Charlotte, North Carolina-based Bank of America, Zurich-based UBS and London-based HSBC declined to comment. Officials at the U.S. Treasury Department also declined to comment on the transactions.

Onshore, Offshore

For decades, rubles and dollars changed hands through the Moscow Exchange — the so-called onshore market — while investors also traded through deals arranged by banks in what’s known as the offshore market. There was little difference until the invasion last year, which stunned investors and triggered a wave of EU and US sanctions. President Vladimir Putin’s regime introduced capital controls in response, such as forcing the country’s exporters to sell their foreign currencies, and a stark split emerged between the two rates.

Wall Street traders were unwilling or unable to exchange currencies directly with Russian banks as a result of sanctions. But for some banks in countries such as Kazakhstan or Armenia, which have kept close ties to Russia since the collapse of the Soviet Union, there were fewer restrictions. For a fee, they could act as intermediaries, buying cheap dollars in Moscow and shipping them to trading desks in London or New York, the people said.

“Third parties like Kazakhstan and Armenia didn’t impose any sanctions on Russia, so they see it as a business opportunity rather than a risk,” said Maria Shagina, who researches sanctions at the International Institute for Strategic Studies in Berlin. “Unless there are clear threats of secondary sanctions, they would be eager to capitalize on this opportunity.”

Clients Clamor

To be sure, buying low and selling high is what Wall Street traders are paid to do and they’re expected to feast on the sudden shifts in asset prices that volatile geopolitics can create. Also, there was no shortage of willing clients, the people said. Large companies were eager to exit Russia and may not have cared about the profits that were being generated for bankers along the way.

“In a fire-sale environment, sometimes you’re happy to get something rather than getting the best price,” said Naresh Aggarwal, associate director at the Association of Corporate Treasurers, a trade body in London. “Their assets had already lost large amounts of money anyway just by virtue of being in Russia. If you lose another 5% because of a high exchange rate, you’re not going to worry about that, but about the 50% loss of the value of the asset.”

Even when the onshore and offshore rates converged later in the year, a gap remained that was big enough for traders to exploit, the people said.

Take May 20 last year. A trader in Kazakhstan might have bought $10 million from a bank in Russia around the onshore rate of 59 rubles per dollar, added on a mark-up of 1 ruble per dollar and flipped them on to a Wall Street counterpart for a quick profit of about $169,000. The Wall Street trader may then have sold them on again to an international client nearer an offshore rate of 61.5 rubles per dollar, perhaps reaping close to $250,000.

This remains an ongoing opportunity for Wall Street banks, the people said, even as the rates have narrowed further. On Wednesday, the ruble traded at around 92.4 per dollar both offshore and onshore at 9:08 a.m. in London.

Wall Street’s ruble arbitrage may have helped their clients manage a chaotic period, said Joseph Pach, a former head of currency trading at a Bank of New York Mellon Corp. subsidiary who now runs San Francisco-based trading firm Corcovado Investment Advisors.

“I see intermediation and providing liquidity as a justifiable practice,” Pach said.

Any assessment is complicated by the different sanctions regimes in different jurisdictions that took effect at various times. But several attorneys said there didn’t appear to be a sanctions violation.

“All those banks will be very heavily lawyered up,” said Anna Bradshaw, a London-based sanctions partner at the law firm Peters & Peters. “It’s difficult to see how they could at that stage have collectively engaged in that without a lawyer at at least one of those banks going bananas if there had been a sanctions breach.”

First Leg

The Russian banks involved in the first leg of the trade included Gazprombank PJSC, the Moscow-based financial-services arm of the sanctioned state-owned gas giant, the people said. The US Treasury Department’s Office of Foreign Asset Control imposed sanctions on its entire management board last year. AK Bars Bank PJSC, a large regional lender based in Kazan in the oil-rich region of Tatarstan, has also been involved, the people said.

Emails requesting comment from Gazprombank and AK Bars weren’t returned.

Raiffeisen Bank International AG, the Austrian lender with a large Russian presence, also has been one of the most active sellers, the people said. The Vienna-based firm, which handles a sizable portion of all euro and dollar transactions in and out of its eastern neighbor, cited “extraordinarily high” income from trading currencies including the ruble last August.

A spokesperson for Raiffeisen, which said Tuesday it was continuing efforts to downsize its Russian operations, declined to comment.

Playing the Middle

The arbitrage was also lucrative for the Kazakh and Armenian banks that played the middleman role.

Halyk, which is controlled by a daughter of former President Nursultan Nazarbayev and her husband, made 173 billion tenge ($390 million) from FX operations in 2022, more than the past four years combined, according to company filings.

Jusan, which was also linked to Nazarbayev in the past but recently changed ownership after a legal battle, reported almost 49 billion tenge on a consolidated basis, a more than 290% annual surge. The banking subsidiary of Kaspi, a financial-technology giant controlled by billionaires Vyacheslav Kim and Mikheil Lomtadze, more than doubled income from the trading business to almost 36 billion tenge, filings show.

Representatives for Kaspi said the company serves local merchants and retail consumers in the ordinary course of business. The banking subsidiary generated $8 million of revenue from trades involving the dollar and the ruble in 2022, or about 0.4% of total revenue, a spokesperson said.

Flight Money

It’s impossible to tell how much of these gains were as a result of trading with Wall Street banks. Russians have sent some $43 billion of their savings overseas since last year and much of it went to bank accounts in nearby countries including Kazakhstan, Armenia, Georgia and Azerbaijan. Still, the ruble arbitrage played an important role, the people said.

In Armenia, profits from spot FX transactions at Ameriabank more than quintupled to 42 billion dram ($109 million), filings show. Ameriabank is controlled by Ruben Vardanyan, once a leading figure in Moscow’s financial scene who co-founded and led the Troika Dialog investment bank.

“FX gains from USD/RUB arbitrage transactions constituted a modest share of the income from FX transactions in 2022,” spokesperson Artyom Mkrtchyan said. “Ameriabank’s arbitrage transactions have been predominantly conducted with western institutions in both legs.”

These kinds of arbitrages are common when a country imposes restrictions on foreign exchange, said Francis Breedon, former head of FX research at Lehman Brothers Holdings Inc. and now a professor at Queen Mary University of London. Even still, Breedon said, Wall Street’s ruble arbitrage is out of the ordinary.

“What seems unusual in this case is the scale and ease with which it is being done,” Breedon said.

--With assistance from Jenny Surane, Irina Reznik, Jake Rudnitsky, Marton Eder, Sara Khojoyan, Helena Bedwell, Srinivasan Sivabalan, Katherine Doherty and Mark Cudmore.

Author: Donal Griffin, Nariman Gizitdinov and William Shaw