The barrage of fresh Treasury bills poised to hit the market over the next few months is merely a prelude of what’s yet to come: a wave of longer-term debt sales that’s seen driving bond yields even higher.

Sales of government notes and bonds are set to begin rising in August, with net new issuance estimated to top $1 trillion in 2023 and nearly double next year to fund a widening deficit. The Treasury is already in the middle of an estimated $1 trillion bump in bills as it seeks to replenish its cash coffers in the wake of the debt-limit deal.

It’s an explosive mix for borrowing costs as debt sales are swelling and the Federal Reserve continues to reduce its balance sheet at a time when traditional buyers of Treasuries overseas are discouraged by currency hedging costs.

“A worsening fiscal profile, amid fairly modest spending cuts, suggests that the upcoming supply deluge will not be limited to T-bills,” wrote Anshul Pradhan, head of US rates strategy at Barclays Plc. “The Treasury will soon need to increase auction sizes meaningfully across the curve. We believe the rates market is too complacent.”

Barclays strategists predict the net rise in coupon-bearing debt from August to year-end will be nearly $600 billion. And that would only ramp up in 2024, they say, with an annual figure of $1.7 trillion. That would be nearly double this year’s expected debt issuance.

Pradhan says he doesn’t think the market appreciates the increase in issuance that’s going to be needed due to wide budget deficits and the fact the Treasury won’t want bills to become a substantial share of the total debt.

Total net new bill sales are set to bring their share of US debt to about 20%, according to JPMorgan Chase & Co. The issuance would hit a threshold seen by the Treasury Borrowing Advisory Committee as the upper limit for the US to fund deficits at the least possible cost to taxpayers.

Bank of America Corp. says the supply deluge could result in a “demand vacuum” for longer maturity bonds that could push yields higher and tighten financial conditions.

Treasury Jacks Up Bill Sales to Bolster Cash After Debt-Cap Deal

Another point of pressure is the fact that demand from traditional buyers like US banks and foreign accounts has been waning.

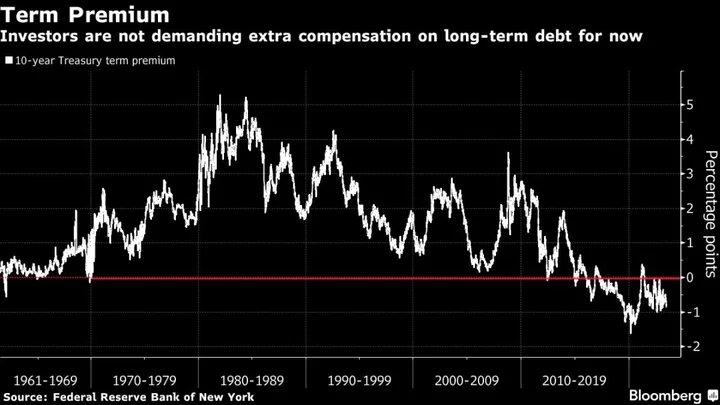

For JPMorgan, that will likely force the Treasury to rely on more “price-sensitive buyers” like hedge funds and asset managers. That could mean a “higher term premium, narrower swap spreads and a steeper yield curve,” said Jay Barry, head of US government-bond strategy at the bank.

Term premium is the extra compensation investors demand to hold longer-term Treasuries rather than rolling over short-dated obligations. It was positive until it went below zero in the post-financial crisis era as the Fed’s role in the marketplace grew. The 10-year term premium is currently about -0.88 percentage point, according to a New York Fed model.

Treasury Flags Bigger Sales as Soon as August, Buybacks in 2024

Meghan Swiber, rates strategist at BofA, says the combination of the added supply and still positive US growth is problematic.

It “creates more question marks around who is the buyer base, especially if there is no recession,” Swiber said. “The largest threat to this coupon supply being absorbed smoothly is a soft landing for the economy or the Fed adding more rate hikes.”

The US central bank remains intent on taming elevated inflation, and while June saw a pause in its interest-rate hikes, officials forecast more hiking by year-end. The Fed is also tightening policy by shrinking its bond portfolio by as much as $95 billion a month, including $60 billion of Treasuries.

And given the strength of the US currency, global investors face much higher costs to hedge away dollar-exposure risk of buying Treasuries and also for the first time in decades have appealing rates on local debt securities.

“Hedging the currency isn’t going to work right now because hedging costs are expensive,” said Hideo Shimomura, senior portfolio manager at Fivestar Asset Management Co. in Tokyo. “Almost nobody is doing that in Japan.”

The Search for Lessons From Another US Banking Crisis: QuickTake

Amy Xie Patrick, a Sydney-based money manager who helps oversee the Pendal Dynamic Income Trust, adds that “there are attractive enough rates closer to home where you don’t need to worry about whether you’ve got foreign-exchange risk.”

Ahead of the coming debt deluge, Treasury yields across the curve remain below their recent peaks, but have been trending upward from their lows of March when bank failures sparked a flurry of haven demand.

Two-year Treasury yields are just below 5% and the global benchmark 10-year yield hovers at about 3.72% — well below last year’s high of over 4% — but deeply discounted versus short maturities as the curve is inverted.

US bond yields are being capped for now amid signs of some slowing in growth and inflation easing from its peak, but the debt clock is ticking, said Jim Cielinski, global head of fixed income at Janus Henderson Investors.

“It’s a slow burn,” Cielinski said. Additionally, “the interest rate bill is going to be much higher in the next three years. And excess global savings are dropping as the supply of debt goes up.”

--With assistance from Yumi Teso.

(Updates Treasury yields.)

Author: Liz Capo McCormick, Michael Mackenzie and Ruth Carson