Bulging sales of US Treasuries are about to deliver a major test of investor demand and determine whether a selloff has room to run as the market braces for the biggest round of refunding auctions since last year.

Yields have surged since late July, and climbed again Monday, amid evidence of a resilient US economy, and after the Treasury shocked traders last week when it signaled greater borrowing needs. A rising US budget deficit and a poor fiscal outlook at a time of near full employment contributed to the move by Fitch Ratings to strip the US of its top rating last week.

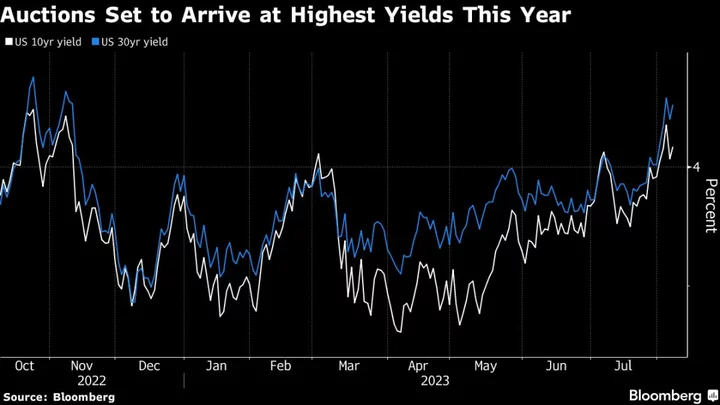

The bond market has to absorb a combined $103 billion of 3-, 10- and 30-year auctions before the week is out — up $7 billion from the May slate — as well as a key inflation reading Thursday. Yields on 10- and 30-year Treasuries are around 20 basis points or more higher than just a couple weeks ago and are within sight of multi-year peaks set in October.

“There are a lot of factors coming together to push long-end rates higher,” Oksana Aronov, head of market strategy at JPMorgan Investment Management, said on Bloomberg TV. The move could have legs, she said, citing the boost to Treasury auctions, a Bank of Japan policy shift and European Central Bank tightening.

The key question is whether long-dated yields above 4% will prove attractive for buyers and also arrest the recent trend toward a sharply steeper yield curve, which has hurt widely-held wagers on a flatter one. The week’s auctions sales start with $42 billion of three-year notes on Tuesday, followed by $38 billion of 10-year notes Wednesday. A $23 billion sale of 30-year bonds on Thursday comes a few hours after the release of the July consumer price index report.

The three-year yield was little changed at 4.46% in Asia on Tuesday, about seven basis points lower than the yield at the July auction for the maturity. The 10-year yield declined two basis point to 4.06%, compared with the 3.86% at last month’s sale.

Tail Pattern

Ahead of each sale, the market is expected to push yields higher to draw in more buyers and leave primary dealers holding less paper to unload after the auction. Sales of 10-year notes have “tailed,” with tepid demand leading to higher-than-expected yields, for the past five auctions.

“Bond markets in general are pretty adept at adjusting in advance of supply,” said Stephen Bartolini, senior portfolio manager for fixed income at T. Rowe Price. “An orderly tail is fine — the important thing is that it’s not enormous.”

Much of the attention will likely fall on how the 30-year fares. The morning of the sale, the July consumer price index is expected to show annual core inflation easing to 4.7% from 4.8%, a level that was eclipsed in 2021 for the first time in decades.

“Of all the auctions this week, I have some concern about how the 30-year bond auction will go, given the sharp rise in yields last week,” said Subadra Rajappa, head of US interest rates strategy at Societe Generale SA. “Following the Fitch downgrade, consumer price data due on Thursday will dictate investor demand for the long-end.”

T. Rowe’s Bartolini said the market could be wrong-footed by expecting CPI to moderate.

“There is an asymmetric risk around the CPI report as the market expects it will show inflation is cooling,” he said.

What Bloomberg Intelligence Says...

“With our updated coupon forecasts for further $1 billion per month to be announced at the next refunding, gross issuance won’t quite return to pandemic funding levels, though may come close. Deficits remain relatively high, but debt runoff and non-marketable debt needing to be funded will make large auction sizes necessary.”

— Ira F. Jersey and Will Hoffman, BI strategists

Click here to read the full report

Beyond the auctions, a worrisome aspect of the latest selloff is that it’s been powered by inflation-adjusted, or real, yields. That suggests the market sees a sturdy economy potentially pushing the Fed to keep policy tighter for an extended period. Aside from the dim US fiscal outlook, the Bank of Japan’s policy tweak late last month, to loosen its grip on Japanese government bond yields, also suggests investors need to price in a higher risk premium for owning long-dated sovereigns.

It all puts pressure on a trade that has favored owning 10-year notes at lower yields for much of this year. Futures positioning data show that asset managers have kept adding to long positions, a stance that is vulnerable to short-covering, according to Bank of America Corp. strategists.

“The swiftness and unexpected nature of yields moving higher means there’s still more unwinding of the long duration trade to come,” said T. Rowe’s Bartolini.

--With assistance from Garfield Reynolds.

(Adds latest yields in sixth paragraph.)