The photo-op was meant to project an image of unity: Thailand’s new prime minister and his central bank governor engaged in a working lunch at the palatial government office in Bangkok.

But the 45-minute meeting on Monday — publicized prominently on social media by Prime Minister Srettha Thavisin after weeks of speculation over brewing friction — has failed to soothe worries over policy disagreements that sent Thai stocks and bonds to fresh lows this week.

At the heart of the tensions is Srettha’s plan to turbo-charge Southeast Asia’s second-largest economy by ramping up spending, subsidies and wages — the centerpiece of which is a $15 billion cash handout program. Bank of Thailand Governor Sethaput Suthiwartnarueput has called such spending “inappropriate.” Just days before meeting the prime minister, the central bank raised interest rates to the highest level since 2013 as a preemptive action to ward off inflation pressure partly from the stimulus.

While the two agreed to meet every month to find a common ground, their remarks subsequently point to no imminent reconciliation. A day after the meeting, Srettha signaled a preference for a weak currency to help exports and tourism — the bedrocks of Thailand’s economy. Hours later, the BOT said it would intervene to curb extreme currency volatility.

Frictions between governments and central banks aren’t unusual, not the least in Thailand. In 2001, then Prime Minister Thaksin Shinawatra, Srettha’s friend and political ally, fired the central bank governor after the official who had been well-regarded by investors for steering the economy through the Asian crisis resisted raising interest rates as he wanted.

But the current discord comes at a perilous moment for Thailand, which is transitioning from a decade of military rule. The nation’s currency is again hurtling toward a 16-year low and Thai stocks have tumbled more than 13% this year. Bond yields have soared to their highest since May 2022. A prolonged stand-off between the policymakers may further aggravate a selloff that’s seen foreign investors withdraw about $1.7 billion from the country since Srettha’s election in August.

Undermining Confidence

“There is a risk that if it continues, it could undermine confidence in the country and could lead to falls in financial markets,” Gareth Leather, an economist at Capital Economics Ltd., said in reference to the rift.

An investor confidence index — which predicts market conditions over the next three months — fell to a neutral zone with an across the board weakening of sentiments, the Federation of Thai Capital Market Organizations said Friday. The gauge fell 20.6% to 112.14 last month as fund outflows and slower economic growth weighed on investors.

How the former property tycoon resolves the dispute will also be seen by investors as a test of Srettha’s leadership given his lack of political experience. His ambitious target to lift growth to 5% or more annually is tied to the planned massive state spending and he can ill-afford to have the central bank not back up his efforts.

Firing a Thai central bank chief is rather difficult after a 2008 amendment to the central bank law conferred BOT more independence. An incumbent governor can be axed only on charges of serious misconduct or malfeasance in discharging duties.

“Both sides seem to be taking extreme positions, which doesn’t help,” Leather said. “Hard to understand why the BOT is so worried about price pressures, given how low inflation is. Similarly, the aggressive loosening of fiscal policy is probably unnecessary given the economy is still doing well.”

Headline inflation has remained below the central bank’s 1-3% target range for five months in a row, while the economy is forecast to expand 2.8% this year, the fastest pace of expansion since 2018.

Investors are concerned about the cost of boosting growth and the wider fiscal deficit that it may trigger, not to mention the lack of clarity on how the government plans to finance them.

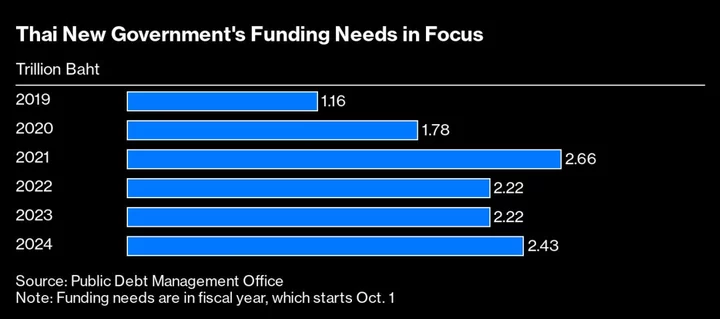

The government may need 700 billion baht ($19 billion) to fund its programs next year, the Thailand Development Research Institute estimates. Such spending poses risks to the sovereign credit ratings and can elevate public debt levels apart from stoking inflation, Kirida Bhaopichitr, an economist at the institute says.

“What has happened may raise questions about fiscal-monetary synchronization and central bank independence” Kirida said. “It may hurt confidence of investors who look from outside,” she said.

Whether Srettha and Sethaput eventually work it out remains to be seen. For now, differences are bound to persist.

“The prime minister is wearing his hat and I am wearing mine,” the central bank governor told reporters on Wednesday, referring to their different roles. “So it’s not surprising that we have some disagreements. But it doesn’t mean we can’t work together. There is no such thing as a conflict.”

(Updates with details of investor sentiment index slump in eighth paragraph.)