SoftBank’s mooted plan to move into private credit is the latest sign the market’s having what Blackstone Inc. President Jon Gray calls a “golden moment.”

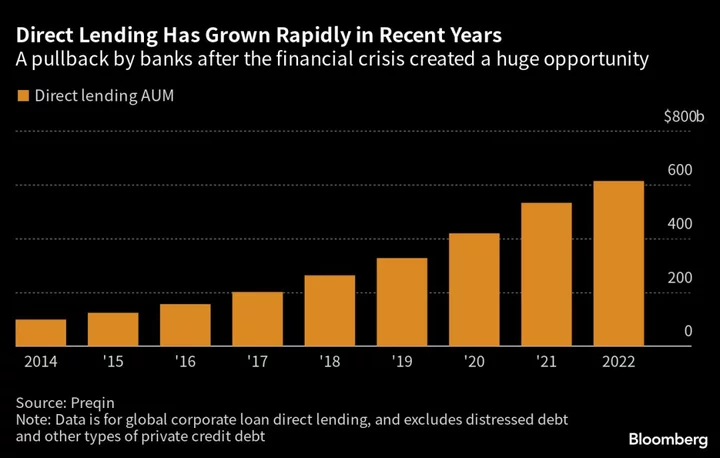

Rising interest rates are making the returns even more attractive for credit providers and a pullback by banks means there’s less traditional competition. This week saw asset managers such as BlackRock and Allianz point to the strengths of the $1.5 trillion asset class, while private equity firms are looking to expand their offerings.

“You’re getting paid north of 10% depending on the type of company,” said Apollo Global Management Co-President Jim Zelter of the opportunity.

The fact that SoftBank, one of the world’s most aggressive tech investors, is looking at private credit is more evidence of the market’s rapid growth and its increasing ability to fund large acquisitions. Multi-billion dollar debt deals for firms such as Zendesk Inc. and Coupa Software have been funded by direct lending in the past year.

Read more: Apollo Swells Ranks in UK and Europe as Private Credit Booms

While new loans are proving profitable for non-bank lenders, some existing deals look set to come under pressure. Private credit providers offer floating-rate debt — meaning margins are tied to base rates — and with higher for longer benchmarks now becoming a reality, there’s a risk that companies will not be able to service their interest bills.

Historic default rates of 2% to 3% “may be challenged by companies that are having higher interest costs across the board,” Zelter said in the interview on Bloomberg TV. Some businesses should be able to pass on higher expense through price rises, he said, but it will cause difficulties for others, particularly those that didn’t hedge their risk.

Listen to: Inside the Private Debt Boom; Korea Bank Stress: Credit Edge

There are limited ways of trading out of private loans, so credit difficulties can prove costly for the providers. As a result, firms including HPS Investment Partners and Bain Capital are beefing up their restructuring teams in anticipation of stress emerging in their portfolios.

The higher cost of borrowing means buyers will not be able to pay as much as they were for companies while some small- and medium-sized businesses may face a credit crunch following the regional banking crisis in the US, Lazard Chief Executive Officer Kenneth Jacobs warned on an earnings call last month.

Capital “is just a lot more expensive today” than it was in 2021, said Jacobs, who will become executive chairman of the firm later this year.

The demise of Silicon Valley Bank, a key lender to tech firms, may also affect credit availability to the startup scene.

That means private credit could be a potential boon for SoftBank after a slump in its equity investments led S&P Global to downgrade its debt to BB, a decision it termed “extremely regrettable.”

The Japanese bank sees an opportunity to use its existing expertise in the tech space, this time through providing credit. Senior investors at the firm have spoken to industry players about the possibility of deploying as much as $1 billion of debt via its venture capital unit, Bloomberg News reported this week.

Elsewhere:

- The leveraged loan market is on track to hand investors the biggest losses on record for defaulted debt, Lisa Lee writes. Loans have been trading for around 22 cents on the dollar after defaults this year, far below the 70 cents that leveraged loan investors have historically recovered from busted companies. It’s another example of fallout from the era of easy money in which money managers gave up safeguards.

- Private equity firm CVC Capital Partners is ramping up its capital markets business to start underwriting debt used to fund buyouts. The move would align it with a growing roster of firms that already finance their own deals by providing and selling a share of the debt, including KKR, Apollo, Blackstone, Carlyle and EQT.

- Banks are readying a roughly $5.5 billion debt sale to support Apollo Global Management Inc.’s acquisition of Univar Solutions Inc., the latest test of investor appetite for risky loans and bonds that back buyouts. JPMorgan Chase & Co. is leading the loan and bond financing and plans to launch the offering to investors in early to mid June, people familiar with the matter said.

- Banks’ preferred shares are recovering from the hit they suffered when a handful of regional lenders in the US imploded earlier this year, with some investors starting to scope out the market’s price discounts. An index of financial-company preferred shares, a type of security that combines elements of equity and debt, has climbed more than 4% to 174.69 this month since falling to a three-year low on May 4.

- A group of first-lien lenders to Mallinckrodt Plc has pitched a proposal to the drugmaker that would allow them to bid for the company’s assets through another bankruptcy as a $200 million payment owed under its settlement in the opioid crisis comes due, according to people familiar with the matter.

- China’s conglomerate Wanda, the latest property-related firm in the nation that plunged into distress, is racing to defuse a liquidity crunch and potential confidence crisis by mulling shopping mall sales in some wealthy provinces and debt buyback, moves that led to a surge of the dollar bonds.

- Debt worries of China’s local governments continue to spread after a financing vehicle in the southwest Yunnan province made a rare late bond payment. Other local-level firms there have also shown strains, as the province’s revenue took a heavy hit by plunged land sales.

- South Korea wants brokerages to swap short-term risky property debt for longer term borrowings, in bid to counter risks in the real estate market and avoid a repeat of last year’s turmoil.

--With assistance from Catherine Bosley, Natalie Harrison, Michael Gambale and Paul Cohen.