Singapore’s financial markets have rapidly switched to a new lending benchmark as the city-state joins the world in saying goodbye to the discredited London interbank offered rate.

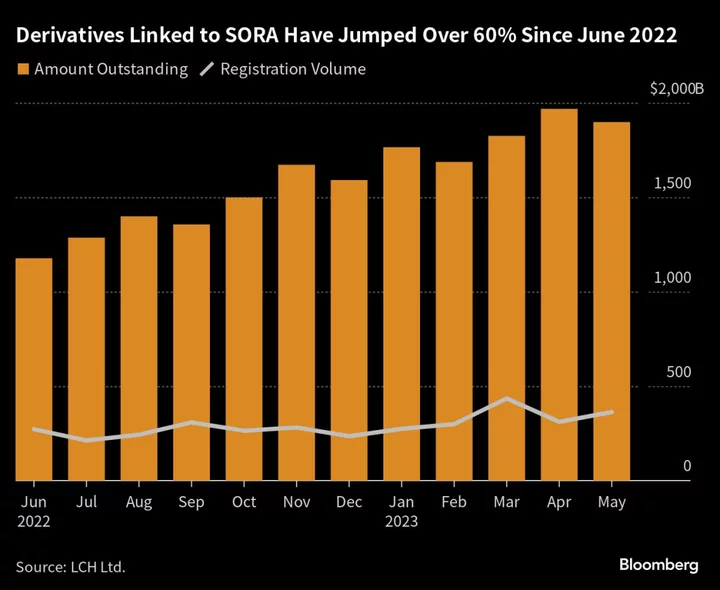

The outstanding value of index swaps pegged to the Singapore Overnight Rate Average — or SORA — climbed to almost $2 trillion at the end of May, more than 60% higher than in June 2022, data from clearing-house LCH Ltd. show. For loans, the total outstanding climbed to S$171 billion ($126 billion) in December, according to the local banking association.

The new gauge replaces the Singapore dollar swap offer rate, known as SOR. It got computed using Libor, which is being published for the last time on Friday.

“Singapore has been preparing for this transition and it should be a smooth one,” said Selena Ling, head of treasury research and strategy at Oversea-Chinese Banking Corp. “There is a robust infrastructure and process in place.”

Policymakers around the world have been introducing new gauges to replace Libor — a decades-old reference rate for bonds, loans and other forms of credit — following evidence from as early as 2008 that it had been manipulated by its contributing banks.

A number of non-US dollar Libor rates were discontinued in January 2022, and all remaining dollar Libor ones will cease to be published after June 30.

Since Libor was a global benchmark, getting rid of it is “chipping away a little bit further of the dollarization of the global economy,” said Stuart Cole, chief macro economist at Equiti Capital UK Ltd. While the shift take into account regulators’ concerns, “you’re going to get this continual fragmentation, and all that does is raise costs and destroy liquidity,” he said.

SORA, administered by the Monetary Authority of Singapore, is the volume-weighted average cost of borrowing Singapore dollars on the interbank market overnight. The gauge is based on actual trades, unlike Libor, which was liable to rigging because traders could submit fake bids.

A significant majority of derivatives tied to the SOR have now switched to SORA, MAS said this week.

SOR is an implied interest rate that relies on Libor input to reflect the cost of borrowing US dollars and converting them into local currency. The amount of outstanding SOR derivatives slid to S$400 billion in March from more than S$3 trillion in late 2019, while SOR corporate loans fell to S$21.7 billion from S$114 billion, the Association of Banks in Singapore said last month.

The Association of Banks also said it would discontinue SOR as planned after June 30, despite the UK Financial Conduct Authority’s announcement that it would require the publication of synthetic US dollar Libor until Sept. 30 next year.

All SOR users should aim to either actively transition away from the gauge, or insert appropriate contractual fallbacks into their contracts that mature after June 30, the association said. It released guidance on adjusting spreads for legacy debt tied to SOR earlier this month.

New Guidance

“To our knowledge, there are no significant issues outstanding with regard to the approaches by which SOR exposures should be converted to SORA,” MAS said. Retail loans pegged to SOR were automatically converted to SORA in October last year.

The Singapore interbank offered rate — or Sibor — another local lending rate similar to Libor that is most commonly used in the small- and medium-sized enterprise and retail loan markets — will be discontinued by the Association of Banks at the end of next year.

--With assistance from Tania Chen, Masaki Kondo, Paul Jackson, Aline Oyamada and Daedo Kim.

(Updates with quote in fourth paragraph, fresh detail on Korea’s transition in box)