Faced with only limited signs of a slowdown in US demand despite more than five percentage points of interest-rate hikes, logic would say the Federal Reserve needs to do more.

But policymakers and Fed watchers are now giving more attention to a new line of argument, that central banks need to take account of what their actions mean for the supply side of the economy. The implication: Too-high rates could actually undermine the inflation fight, by squelching the benefits of increasing supply — which are just now coming on stream.

It’s a cornerstone of macroeconomic theory that monetary policy works mostly on demand. Raise rates, borrowing gets more expensive, and demand falls — damping inflation. Recessions are the ultimate tough medicine for too much demand and getting prices under control.

But a group of frontier economists is warning that monetary policy can have an important impact on supply, which influences the economy’s longer-run trends. Fed Chair Jerome Powell and central bankers from around the world heard the argument in a key paper at the annual Jackson Hole symposium last month.

Evidence shows that interest-rate surges affect financing conditions and the appetite for risk, constraining the supply side of the economy by inhibiting innovation, Yueran Ma and her co-author Kaspar Zimmermann found in the paper.

Powell himself at the conference highlighted the role of supply as a vital complementing factor to demand.

“While these two forces are now working together to bring down inflation, the process still has a long way to go,” the Fed chief said Aug. 25. He said that in addition to waiting for the pandemic demand surge and supply constriction to unwind, Fed policy was designed to “slow the growth of aggregate demand, allowing supply time to catch up.”

Powell will have the opportunity of discussing the two dynamics on Wednesday, in his press briefing following the Fed’s latest rate decision and policymakers’ updated projections for the benchmark rate. Economists anticipate no change in rates this time, with the potential for officials to pencil in one more move later this year.

Wage gains have been cooling in recent months as strong economic growth boosted participation in the workforce, helping solve labor shortages and moderate wage increases. A similar development has arguably been occurring with consumer prices.

Bigger Role

“The majority of disinflation has been driven by expanding supply rather than decreasing demand,” Mike Konczal, director of macroeconomic analysis at the Roosevelt Institute, said in a paper published this month.

Persistent demand can be a good thing, helping producers fund investments to reorganize supply chains. And too-tight monetary policy can also be counterproductive for particular sectors of the economy, such as housing — historically high borrowing costs can crimp construction, keeping shelter costs elevated.

It’s a policy paradox for the Fed to consider the role of allowing moderate growth — rather than sharply braking it — in order to get inflation sustainably back to its 2% target over the next few years. (The current core rate is 4.2%.) But that’s the implication of the new research.

“The results show that a tightening shock of 100 basis points on average would be followed by lower GDP” on the order of 1%, the University of Chicago’s Ma said in an email. She highlighted that, in the current Fed cycle, venture capital market-risk appetite “is much lower now than before tightening started.”

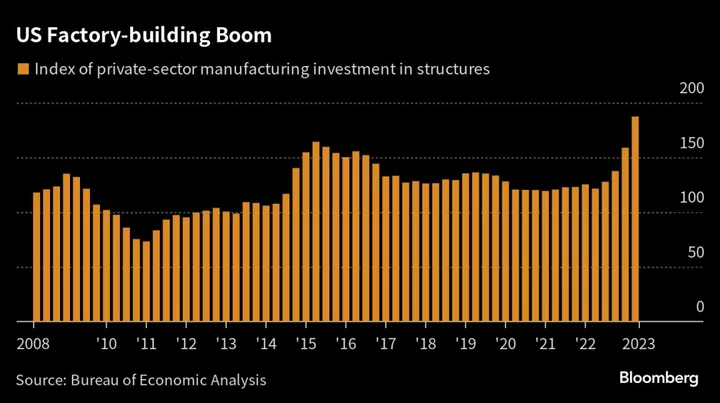

Expanding supply has been one reason for US economic growth clocking 2% or faster in each of the past four quarters, despite the Fed’s rate hikes. Factory construction has almost doubled in the past year, with its contribution to gross domestic product hitting the highest since 1981.

Traditionally, supply was thought to be more a story about the economy’s bedrock structures — like population growth or energy endowments, which are less affected in the short term by the cost of money.

Ma, the co-author of the Jackson Hole paper, flagged a recent study by economists Luca Fornaro of the Barcelona School of Economics and Martin Wolf at the University of St. Gallen.

“If monetary tightening actually makes it harder to reduce marginal costs on the supply side – for example, through slower technological progress or more misallocation — that can make inflationary pressures more persistent,” Ma said in summarizing the takeaway.

Previous Studies

The research builds on previous studies showing how weak economic recoveries can undermine the supply side — by reducing incentives for business investment and crippling the development of labor skills. Former Fed Chair Janet Yellen addressed it in a somewhat controversial speech in 2016, after the financial crisis left America stricken with a slow recovery.

“This post-crisis experience suggests that changes in aggregate demand may have an appreciable, persistent effect on aggregate supply — that is, on potential output,” she said. “The natural next question is to ask whether it might be possible to reverse these adverse supply-side effects by temporarily running a ‘high-pressure economy,’ with robust aggregate demand and a tight labor market.”

The speech was at a time of low inflation. But today, with price rises far above target, Fed officials can’t tamper with their credibility with such explicit language about supporting growth to bolster supply.

Even so, the attention to supply is visible as Fed officials highlight that they don’t want to kill the expansion and throw the economy into a grindingly slow recovery once again.

While Dallas Fed President Lorie Logan in May remarks highlighted the need to keep monetary policy tight even in the wake of an intense banking crisis, this month she sounded a different tone.

“We must proceed gradually, weighing the risk that inflation will be too high against the risk of dampening the economy too much,” Logan said in a Sept. 7 speech.

--With assistance from Alex Tanzi.