Friday’s sizzling jobs report is bolstering the probability of another Federal Reserve rate increase this year, adding to pain in credit markets that are already getting hurt by a year-long jump in yields.

The strength of the US labor market increases the likelihood that the central bank won’t pivot to cutting rates next year. That’s a big negative for corporate America, which has continued boosting its debt levels even as yields have surged over the last year.

Two data points that highlight the extent of corporate trouble: companies have about $425 billion of dollar-denominated junk debt due to mature before the end of 2025, and market yields for speculative-grade bonds are now at least 3 percentage points higher than the average coupon the borrowers are paying on their existing debt.

The higher borrowing costs that many companies face could cut into profits and increase default risk. Rates staying higher-for-longer will likely have some kind of unexpected impact on the economy, Mohamed El-Erian, the chief economic adviser at Allianz SE, said in an interview with Bloomberg TV.

“This is likely to be bad news for markets and for the Fed,” El-Erian said after the US jobs data was published on Friday. “Something is likely to break, probably in the financial markets, but that will spill back into the economy.”

Even before the jobs report, worries about rising yields had shut down new junk bond sales in the US, bringing the first “zero” week since the week ended Aug. 18, according to data compiled by Bloomberg News. That came as the 30-year US Treasury bond this week breached 5% for the first time since 2007, crystallizing just how challenging and expensive it is going to be for some issuers to deal with their debt.

Read More: The 5% Bond Market Means Pain Is Heading Everyone’s Way (1)

“The junk bond market needs to massively reprice to account for refinancing risk with benchmark borrowing rates so high,” said Althea Spinozzi, a strategist at Danish lender Saxo Bank. “I can’t see how the default rate doesn’t rise sharply and there will be stretched balance sheets everywhere.”

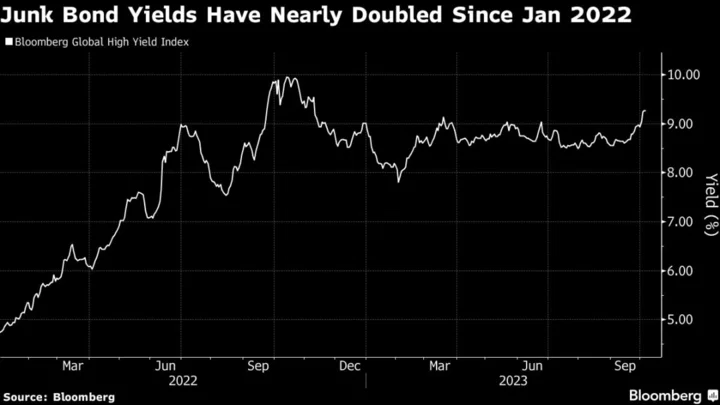

That kind of thinking helped lift the average yield on the Bloomberg Global High Yield index to 9.26% this week, the highest since November last year and nearly double what it was at the start of 2022. The drought in new sales followed more than $23 billion in issuance in September, the busiest month since January 2022.

Economic uncertainty and higher yields make it harder to sell debt. Barclays Plc held preliminary discussions with investors about refinancing a private loan for Hibu Inc., the former Yellow Pages publisher, but found tepid interest from loan buyers and the deal was scrapped. Separately, a planned sale of a portfolio of European leveraged loans worth €290 million ($305 million) was shelved.

Refinancing at higher yields is painful, and many loan borrowers are already feeling heat: benchmarks for the floating-rate debt have been consistently adjusting higher since last year. If rates are higher for longer, then junk bond borrowers face greater risk of having to adjust their coupons materially higher too, said Sinjin Bowron, portfolio manager at Beach Point Capital.

The rapidly growing corporate private credit market will probably also see more defaults, with Bank of America Corp. strategists estimating it could reach 5% next year, exceeding those in the syndicated loan market.

For at least the near term, companies that had planned to come to the market offering risky bonds and loans will probably think again.

“Credit markets are likely to remain under some modest pressure through early November and a combination of earnings blackouts and materially higher borrowing costs should keep issuance fairly limited through October,” said Winnie Cisar, global head of strategy at CreditSights Inc.

Week in Review

- Credit markets took a beating after heading for their worst week since the global banking turmoil in March, with a strong jobs report on Oct. 6 driving Treasury yields to the highest since 2007 and placing more pain on corporate borrowers.

- Private credit funds competing with banks to finance Carlyle Group Inc.’s potential buyout of some units of Medtronic Plc have offered a partial payment-in-kind feature in an effort to win the deal.

- Thoma Bravo is nearing a roughly $1 billion financing package from a group of private credit lenders for its planned acquisition of NextGen Healthcare Inc.

- Apollo Global Management and CVC Capital Partners are among private credit lenders providing €500 million ($526 million) of subordinated debt backing Cinven’s buyout of Synlab AG.

- A group of private credit lenders led by Oak Hill Advisors provided a $505 million loan for Lindsay Goldberg & Bessemer’s acquisition of The Kleinfelder Group Inc.

- Private credit funds are working to provide about a fifth of an up to £1.25 billion ($1.5 billion) financing to back the potential buyout of the UK’s Iris Software in payment-in-kind debt.

- Blackstone Inc. committed $1.5 billion to help finance the merger of HealthComp Holding Co. and Virgin Pulse.

- T. Rowe Price Group Inc. and Oak Hill Advisors are launching a new private credit fund open to individual investors in the US to take advantage of the rapidly-growing $1.5 trillion market.

- BlackRock Inc. is tapping the private credit market to launch a new fund that will offer one of the fastest growing ESG investment strategies in the US.

- Private credit funds have been raking in bonanza profits lately as a result of rocketing interest rates, but their investors are starting to question whether they really deserve so much of the windfall.

- KKR & Co. sees more investors permanently allocating to private credit alongside other fixed-income assets even as public credit markets regained some strength in recent months.

- Sunac China Holdings Ltd. won court approval for its multibillion-dollar offshore debt restructuring plan, clearing the last key hurdle for it to become the country’s first major developer to overhaul such liabilities.

- China SCE Group Holdings Ltd. said it will appoint external advisers and explore a holistic debt plan after not making a $61 million loan payment.

On the Move

- RBC Capital Markets’ head of US credit sales, John Maggiacomo, has left the bank after six years.

- Nikunj Gupta has joined HSBC as head of credit structuring.

- Apollo Global Management Inc. managing director Tiffany Gallo has left the firm.

- Navis Capital Partners recruited Jack Ng as director based in Singapore for its private credit business.

- Veteran debt trader Omar Ghalloudi joined boutique London-based investment bank KNG Securities from Credit Suisse Group AG.

--With assistance from Olivia Raimonde, James Crombie and Dan Wilchins.