One of the year’s top fixed-income trades is facing a critical juncture in Latin America as bond investors attempt to time pivots in US and local interest rates.

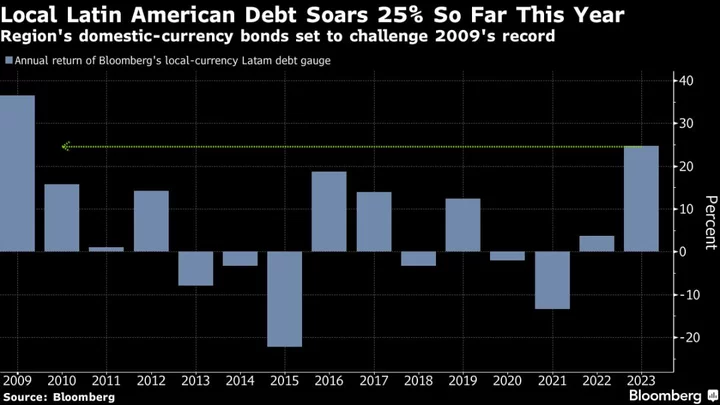

Central banks in the region have wooed money managers with their early and aggressive monetary tightening cycles — establishing a level of inflation-fighting credibility that’s fueled a 25% rally in domestic bonds. Now, as local policymakers start to pivot ahead of the Federal Reserve, the bet comes with a new undertone of risk.

“EM local markets have been the trade of the year,” said Mauro Favini, a senior portfolio manager at Vanguard who was bullish on Latin America earlier this year. “But the road ahead is likely to be uneven and full of bumps.”

The risk, Favini said, is that traders have already priced in central bank easing across emerging markets at a time when there’s less certainty about US rate cuts. The Bank of Japan’s latest policy shift is also opening the door to a stronger yen, which could reverberate through currency markets and undermine the so-called carry trade that’s helped power the Brazilian real and Mexican peso.

The question for investors is whether momentum behind Latin America’s local debt can withstand the near-term market ructions. A key gauge of the notes has risen for nine out of the past 10 weeks, leaving bond bulls to contemplate a challenge of 2009’s stellar 36% annual return.

US policymakers last week, however, delivered a quarter-point rate increase and vowed to adopt for a data-dependent approach, reaffirming trader expectations that the US is nearing the end of its tightening cycle as inflation eases. While few currently expect the Fed to hike beyond the current policy band of 5.25% to 5.5%, there are plenty of economic indicators to come before the next meeting in September.

Of course, a potential Fed pause, along with a weaker dollar, would likely create space for emerging-market central banks to also ease and bolster appetite for local-currency bonds.

That sentiment is already sharpening as investors see the likes of Chile, Brazil and Peru adopting easier policy after driving rates well beyond current inflation levels.

“There will continue to be investors stepping into local-currency debt,” said Liam Spillane, head of emerging market debt at Aviva Investors. “A belief that the Fed has finished hiking is another factor that will encourage investors to re-enter EM debt more aggressively.”

Policymakers in Brazil are set to unveil their next policy decision on Wednesday, with economists and traders alike preparing for the start of an easing cycle in Latin America’s largest economy.

The nation’s central bank is expected to lower its key rate by 50 basis points to 13.25% after embarking on its tightening cycle a full year ahead of the Fed. Annual inflation in Brazil eased in mid-July to 3.19%, the lowest level in nearly three years and down from a peak above 12% in 2022.

“Latin America is attractive given regional central banks are set to act first on cuts,” said Brendan McKenna, an emerging-markets economist and FX strategist at Wells Fargo in New York. “I think positioning now — ahead of the Fed cuts and the dollar downtrend picking up pace — makes sense.”

For T. Rowe Price, the key will be how aggressively Brazil can cut rates in the coming months — especially if the Fed proves reluctant to ease its own policy.

“Brazil is like the US in that they have been hiking and pushed policy to a high level, but the economy is doing well,” said Richard Hall, a sovereign debt analyst at the asset manager. “It’s an interesting question as to whether Brazil may have to stay at elevated rates for a while.”

While T. Rowe remains overweight on Brazil, the firm has pared some of its exposure amid the recent rally, Hall said.

The same danger exists in other emerging markets, too, if inflation remains high and limits the scope of domestic central banks to lower their borrowing costs too aggressively, said Jack McIntyre, portfolio manager at Brandywine Global Investment Management.

“If your starting point is high real policy rates, you should be reducing interest rates, just don’t take them close to where inflation is running,” he said. The firm is paring back its exposure to local-currency debt due to high valuations.

Eyes on Fed, BOJ

The outlook for central bank policy and local debt becomes more opaque outside of Latin America. For Pacific Investment Management Co.’s Lupin Rahman, much of it will come down to the path of the Fed and other major central banks.

Poland will likely start its easing cycle in September and South Africa will initiate cuts later in the year, according to Rahman, the firm’s global head of emerging-market sovereign credit.

Assets from South Korea and Indonesia, meantime, also stand out as their central banks appear positioned to lead Asia’s rates lower, said Eugenia Victorino, head of Asia strategy at Skandinaviska Enskilda Banken AB.

“Central banks will likely cut gradually, mindful of their currency performance and cautious not to disrupt the carry trades that have been romancing the US soft landing narrative,” Pimco’s Rahman wrote in a note.

That came into view last week as the Bank of Japan opted to allow 10-year yields to float higher, beyond its longstanding cap of 0.5% to a limit of 1%, testing emerging-market sentiment in Asia.

The move calls into focus the yen carry trade, which consists of borrowing cheaply from Japan and parking the proceeds in a currency with much higher interest rate. Stellar gains in the Mexican peso and Brazil’s real lately suggest any rebound in the yen from the BOJ’s shift could spur currency volatility — and in turn weigh on returns for local-currency debt.

Of course, it’s also possible that “the carry is still so much in favor of Latam EM even if the BOJ does something,” said Brandywine’s McIntyre.

What to Watch

- Pakistan’s central bank is expected to raise rates by 100 basis points to 23% to meet bailout terms from the International Monetary Fund. The nation will also release inflation data.

- The Bank of Thailand will likely follow through on its messaging and deliver one last hike, with Bloomberg Economics forecasting an increase of 25 basis points.

- Traders will watch China PMIs for signs that the recovery is still struggling.

- Brazil’s central bank may finally start unwinding its very tight monetary policy at its August meeting, while Colombian policymakers are expected to keep a more cautious, data-dependent tone.

- Turkish annual inflation probably accelerated in July, according to Bloomberg Economics, with price gains likely to continue on a rising trajectory through the second half of 2023.

--With assistance from Carolina Wilson, Selcuk Gokoluk and Karl Lester M. Yap.