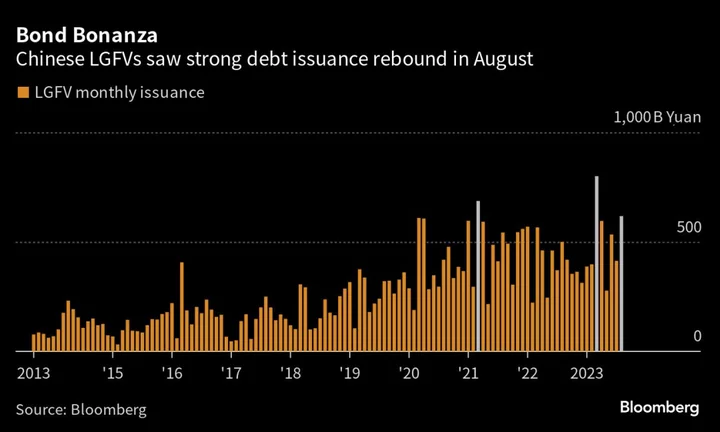

China’s local government financing vehicles are staging a comeback in credit markets, with a surge in yuan bond sales as Beijing intensifies efforts to defuse risks from the debt-laden group of borrowers.

Domestic bond issuance by LGFVs, which are typically tasked to build infrastructure projects, reached nearly 620 billion yuan ($85 billion) in August, an almost 50% jump from July and the third-highest monthly tally on record, Bloomberg-compiled data show.

Driving the boom were financially weaker provinces such as northeastern Heilongjiang, where LGFV bond sales last month totaled eight times more than July’s, with the average coupon down 2.27 percentage points from the previous month. The momentum has continued in September, with a LGFV carrying a low domestic rating of AA pulling off a rare 1.2 billion yuan offering for such borrowers.

The rebound in financing is the latest indication that investors are betting that LGFVs will — for now at least — remain relatively safe as Beijing embarks on a 1 trillion yuan program to help provincial governments repay hidden local debt. That said, most of the bonds sold have short-term maturities, underscoring the lingering concerns about the borrowers’ long-term health as a housing crisis deepens.

“More market participants now believe that the central government will come to the rescue as it won’t allow LGFV bonds to blow up,” said Li Yong, chief fixed-income analyst at Soochow Securities Co. “It’s unlikely that there will be a public bond default by any LGFV within three years.”

LGFVs, some of which have jolted the market with brief payment scares in recent years, have so far avoided delinquencies on public debt.

Echoing the pickup in issuance momentum, LGFV bonds also have shown a turnaround in the secondary dollar bond market. US currency notes from the sector have returned 5% so far in 2023, versus a loss of 0.5% in the same period a year ago, according to an iBoxx gauge.

A notable feature of the latest deal rush is the strong demand for bonds issued by financing vehicles from regions with tighter finances.

A LGFV from one of China’s most indebted cities, Tianjin Infrastructure Construction & Investment Group Co., last month sold a 1.5 billion yuan note due in February 2024 after attracting bids totaling more than 70 times its offering size. The so-called bid-to-cover ratio stands out as it was typically in the single digits for bonds sold by LGFVs from higher-risk areas earlier this year.

Another characteristic is a clear preference among investors for shorter-dated debt, suggesting persistent concerns about the longer-term outlook of a sector that’s heavily exposed to China’s property woes.

This is particularly relevant for the financially weaker regions. For Yunnan, a southwestern province, all of its LGFV bonds issued in August carry maturities no longer than a year. In the indebted northern port city of Tianjin, such notes accounted for 93% of the total.

In the first half of 2023 the average tenor — the length of time before a debt matures — of onshore LGFV bond issuance fell to 2.51 years according to Bloomberg calculations. That’s down from 2.95 years in 2022 and the shortest since at least 1999 when the data series began.

S&P Global Ratings warned in a recent report that the liquidity soundness of lower-tier LGFVs is deteriorating quickly, with a buildup of short-term debt amid depleting cash.

While Beijing’s latest round of policy support may provide a small confidence boost, “the ultimate effectiveness of the new measures hinges on how well they tackle LGFVs’ short-term refinancing challenges while facilitating a long-term debt resolution,” S&P said.

Data from 2022 onwards are calculated based on LGFV bonds issued by the end of 2021, on the assumption that LGFVs that have been set up since then don’t impact the data significantly.

--With assistance from Shuqin Ding.