The bond market’s re-energized bulls may want to dial down their excitement, because their fortunes hinge on whether an abstract, almost elusive number, is as low as they assume.

At the heart of what’s been shaping fixed-income investors’ views this year is the so-called neutral rate, which neither stimulates nor restricts the economy. Treasury bulls began the year invigorated by the belief that the Federal Reserve’s aggressive tightening was set to push borrowing costs well above the neutral level, and that officials would soon have to reverse course.

The bet was that the era of low long-term rates would return and short-dated bonds would rally even faster with central bankers set to pivot to easing before year-end.

Fast-forward to today and the 10-year yield is about where it started January, even after a rally this week sparked by data signaling cooling inflation. The yield curve, meanwhile, isn’t far from its deepest inversion in decades and wagers on 2023 interest-rate cuts have all but vanished.

Firms including Goldman Sachs Group Inc. and TwentyFour Asset Management are taking notice. They’re warning that the neutral rate has increased, and that more Fed officials will eventually acknowledge that trend, tripping up bond bulls and rewarding those who have spurned Treasuries. For Goldman Sachs, the inflation-adjusted — or so-called real — neutral level is as much as four times that implied by the Fed’s long-run projections.

“People haven’t really paid attention to the long-run fed funds rate,” said Felipe Villarroel, a portfolio manager at TwentyFour Asset Management. “We think it’s about to move. It means that the scope for a rally in the 10-year Treasury is more limited as that anchor is higher.”

Data Wednesday showed the annual consumer-price inflation rate has slowed to a two-year low of 3%, fueling speculation that the Fed could wrap up its tightening campaign after one more hike this month. On Thursday, Treasuries extended the rally after a report showed US producer prices barely rose in June from a year earlier.

Still, Villarroel’s argument is also gaining support amid a slew of hot economic reports, from new home sales to consumer confidence. The readings suggest that the Fed’s benchmark rate, already its highest since 2007, may not be restrictive enough relative to the neutral rate. If so, it means the central bank won’t be able to pivot to easing any time soon.

That’s a blow to investors who started the year anticipating a bond-market comeback from last year’s drubbing and amassed, by one measure, the biggest net long position since 2010. Following a 12% slide last year, Treasuries have earned 1.5% in 2023.

More Pain

Former US Treasury Secretary Larry Summers and Bill Dudley, previously the New York Fed chief — are among those who have said bond investors’ pain may not be over, because markets are still underestimating the neutral rate, which is also known as the r-star. Summers is a paid contributor to Bloomberg Television and Dudley is a senior adviser to Bloomberg Economics.

The idea is that forces such as a swelling fiscal deficit, the risk of deglobalization and rising investment in clean energy mean the downward pressures on borrowing costs that persisted for decades may be reversing. It’s a dynamic that marks a departure from the stretch of sluggish growth that capped the neutral rate after the Great Financial Crisis.

“We’ve had 40 years – with exceptions – but with a trend of falling interest rates,” Lara Rhame, chief US economist at FS Investment, said on Bloomberg Television on Tuesday. “Looking ahead, if we get this bounce in r-star, and I think we are seeing it,” it will be difficult for bonds to see price gains.

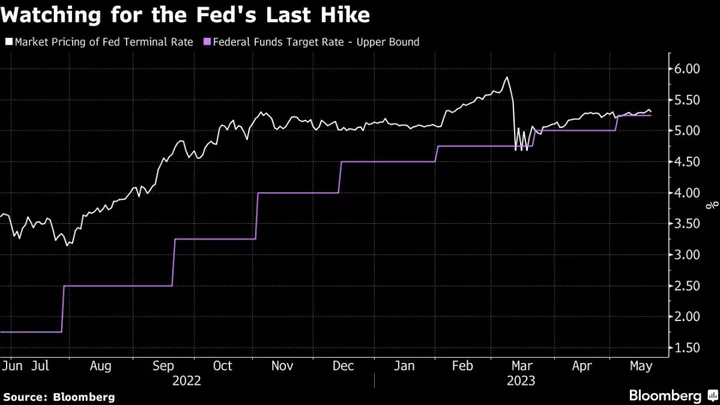

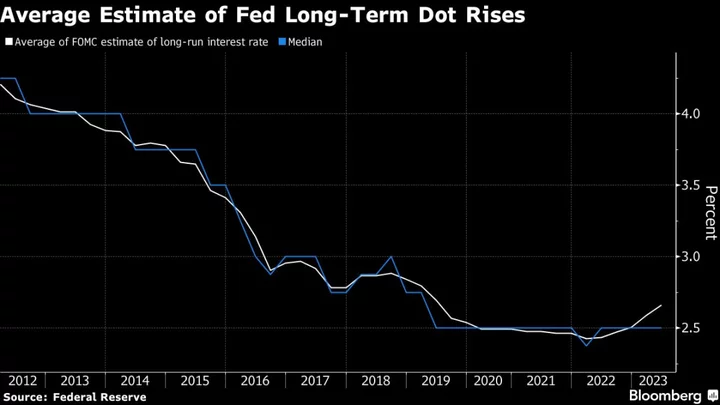

So far, the view on the neutral rate represents the minority. While a small group of Fed officials have nudged up their estimates of the long-run rate, the median – encompassing the majority — remains at 2.5%. Current New York Fed President John Williams and his colleagues essentially backed that view in an update of their model in May.

For his part, Villarroel at TwentyFour Asset Management sees the Fed’s median gradually rising to 3%, likely over the course of about six quarters.

Investors, by and large, don’t anticipate that move. A swaps-based measure of the market’s assessment of the inflation-adjusted r-star is about 0.8%, consistent with the 10-year average before 2020. It’s also not far off the median Fed estimate of 0.5% for the neutral rate after inflation.

For Jeffrey Rosenberg at BlackRock Inc., it’s precisely the difficulty of measuring where the neutral rate is that makes it hard to take an aggressive position in the bond market.

With all the questions around it, “it really tempers the ability for the Fed to cut rates aggressively,” said Rosenberg, a portfolio manager of the firm’s Systematic Multi-Strategy Fund. And that dampens bonds’ role as a hedge, he added.

The neutral rate is also at the center of another market debate — over the deeply inverted yield curve, a widely watched indicator of impending recession. The current low estimate of r-star, the thinking goes, is capping long-term yields, potentially keeping the curve flatter than it otherwise would be.

The result is that the inversion overstates the prospect of an economic downturn, says Praveen Korapaty, chief interest-rate strategist at Goldman Sachs. His estimate for the real neutral rate — in a range of 1.5% to 2% — means that the curve should be about 50 basis points steeper.

“It boggles my mind that we are looking at a very different set of facts, this cycle versus the last cycle, but somehow, magically, there’s this insistence that the level of rates the economy can withstand is exactly the same in both cycles,” he said.

--With assistance from Michael Mackenzie.

(Updates with PPI data, latest market move.)