Private credit funds, backed by some major global investors, are venturing where Australian banks increasingly fear to tread: the country’s precarious property industry.

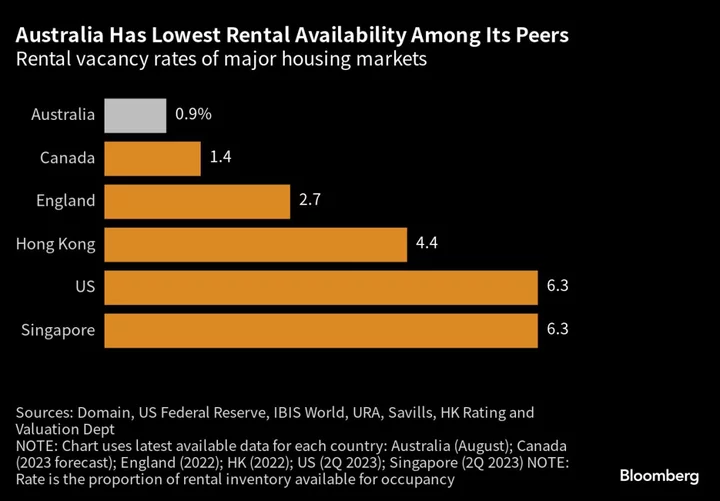

A chronic housing shortage in Australia has spurred real-estate debt funds like Apollo Global Management-backed MaxCap Group Pty to pivot from traditional commercial projects to residential developments, with rental home vacancies at a record low. They’re seizing an opportunity as banks take a cooler approach to real-estate lending that’s soared to A$435 billion ($277 billion).

But while returns on the debt are topping 10% and housing demand seems endless, there are some hefty risks involved. Building firms caught out by surging costs are collapsing at a record pace, with current liabilities exceeding current assets at more than half of all large builders, according to an Australian Constructors Association report in July.

“You do need to be careful about where you choose to invest and who you choose to invest with,” Sam Tamblyn, managing director at Melbourne-based real estate consultant Urban Property Australia, said in an interview. “Do you have confidence in the builder to finish the project?”

More than 2,000 construction firms have entered into administration so far this year, with 785 in the three months through September, according to Australian Securities & Investments Commission data. Many firms that locked in fixed price contracts during the pandemic found themselves in strife when costs escalated, leading to delays in completing projects, while the sector has also been plagued by material and manpower shortages.

That isn’t fazing private credit funds from gauging opportunities, enforcing added risk management across deals to ensure they’re hedged against delays and cost overruns. Apartment projects are also offering an alternative to office investments that have become far more challenging as work-from-home trends persist. For investors, the debt offers a natural hedge against inflation as it’s typically benchmarked against floating-rate interest.

Funds interviewed for this story cited returns averaging 5%-6% over the cash rate, which the Reserve Bank of Australia this week lifted to a 12-year high of 4.35%. They also flagged the appeal of Australia’s economic outlook as immigration rebounds strongly following the pandemic. The central bank on Friday increased its growth forecasts, saying the economy was proving more resilient than previously expected.

“We believe the fundamentals remain strong and highly appealing from a risk-adjusted return perspective,” said Bill McWilliams, chief investment officer of MaxCap, which manages more than A$7 billion of assets. As the country’s big four banks pull back, “we’re seeing the emergence of institutional capital and private capital come into that space to fill that void,” he said.

Australia’s banks are more risk-averse on real estate after the regulator this year imposed stricter capital rules for development and construction loans. Their exposure to commercial property rose by just 0.6% in the June quarter, compared with 2.7% a year earlier, according to Australian Prudential Regulation Authority data that excludes lending to individual homebuyers and investors.

Banks still, however, have a significant stranglehold on commercial property loans at around 90% market share. In North America and Europe, they make up a far lower portion of between 40%-60%, according to real estate fund Qualitas Ltd. That imbalance is a key draw card for big offshore names, said Mark Fischer, global head of real estate.

“Those international investors see the disconnect between Australia and what they have observed and invested successfully in other markets,” he said. “When you look at the total size of the market, even small reductions in the bank participation rate open up a large opportunity set for alternative managers.”

Apollo snapped up a 50% stake in MaxCap in 2021. Qualitas has now secured about A$1.4 billion in commitments from the Abu Dhabi Investment Authority, following the sovereign wealth fund’s most recent A$700 million mandate in August. The firm’s Sydney-listed Qualitas Real Estate Income Fund posted an 8.35% net return for the year through September.

Real-estate debt margins have widened “meaningfully” as liquidity has tightened, offering “equity-like returns” in some sectors of the market, said Jason Howes, fund manager at the asset management unit of Australian landlord Dexus. The firm is raising a second fund focusing on distressed to growth opportunities, with a bias on the residential sector.

Caution is required. Delays have meant financiers can wait longer to be repaid, according to Cathy Houston, managing director of real estate credit at MA Financial in Sydney. Furthermore, the firm has had to replace four builders across various projects in the past couple of years. To mitigate that risk, lenders stress-test the project on the assumption the builder will fail, she said.

“We undertake due diligence on builders, look at the financials, understand what other projects they’ve got on, understand what other debt they have, where those projects are up to and look at the amount of available cash the developers have to fund cost overruns,” Houston said.

Loan-to-cost ratios, which show how much equity the borrower has contributed and are used in agreements to protect against market movements, have also come down within the past 18 months, said MaxCap’s McWilliams.

In the overall commercial property sector, valuations in Australia have held up better compared to the US and Europe, according to Bruce Wan, head of research at MaxCap. “We have seen some private credit distress in the US and Europe because the underlying collateral fell 30% to 50% in office buildings. We have not seen that in Australia.”

Still, Tamblyn thinks valuations across commercial property have further to fall as the central bank’s 13 rate hikes since May last year take time to filter their way through to the economy.

“The increases in interest rates have still got some way to play out and asset prices are still grinding through and they haven’t reached an equilibrium yet,” he said. “There is still more downward pressure to go.”

(Adds updated RBA forecasts in 7th paragraph)