Interest-rate hikes may be peaking in Europe, but for the consumers, companies and governments that borrowed trillions of euros during the era of ultra-low borrowing costs, there’s still plenty of pain in store.Through the end of this decade, borrowers across the continent face repayment on a mountain of debt sold when financing costs were many times lower. Although the adjustment is painful in many places, including the US, it’s a particular shock in Europe, where interest rates were below zero for eight years. Many borrowers have delayed refinancing in the hope that rates would come tumbling down again. But with economies having largely performed better than expected, that’s looking increasingly unlikely.Read More: Lagarde Keeps ECB Rate Debate Raging as Key Figures AwaitedInvestors predict that the coming years will be marked with defaults and spending cuts as a larger portion of corporate, household and state income goes into financing debt. A stark indicator of the approaching sea change is the gap between what governments and companies globally are currently paying in interest and the amount they would pay if they refinanced at today’s levels. Apart from a few months around the global financial crisis, the gauge has always been below zero. Now it’s hovering around a record high of 1.5 percentage points.

“If your bet was the 2010s was the new normal where rates kept falling and you can always refinance, this is a really difficult environment,” said Mark Bathgate, a former Goldman Sachs Inc. and BlueBay Asset Management investor who now runs his own advisory firm. “The issues in European credit could be a lot worse than in the US. There was a lot more scope for excessive leverage to be built up. ” Milton Friedman first coined the idea of long and variable lags in monetary policy in the 1960s. Put simply, it’s the uncertain lapse of time before changes in monetary policy start to impact the economy. While the price of assets such as government bonds often moves in anticipation of, or immediately after, a central bank decision, it takes time for rate shifts to feed into longer-term contracts, and so into price-setting, labor markets and, eventually, inflation. For companies, many of which borrowed heavily during the pandemic, the big refinancing wall starts in 2025 and peaks in 2026. High-yield firms in Europe have over $430 billion of debt due in the second half of the decade, according to data compiled by Bloomberg.

“During the vintage years of easy money there wasn't as much consideration given to what a high interest-rate environment might look like,” said Danielle Poli, a portfolio manager at Oaktree Capital Management. “We still see stress brewing ahead for some borrowers, especially those that have more aggressive capital structures.”

To be sure, defaults among the riskiest companies aren’t expected to get anywhere near the 13.4% rate seen during the global financial crisis. Moody’s Investors Service forecasts that the global default rate for junk-rated companies will surpass the historical average by the end of this year, before peaking at 4.7% in March 2024. For Europe, it's predicted to peak around 3.8% in the middle of next year.For most firms, higher rates are more likely to lead to a drop in capital expenditure, which in turn will weigh on economic growth. Companies in Europe, the Middle East and Africa bought back bonds at the fastest pace since 2009 in the first five months of year to trim leverage and cut interest payments. Others have sought to lengthen the maturity of their existing debt. While this is often sweetened with a pick-up in the coupon, it’s cheaper than going to the market and attracting new investors with a fresh debt issue.

Bank of England researchers estimate that highly-leveraged companies account for around 60% of UK corporate debt, but only 5% of the cash. This means these firms are more likely to reduce investment or jobs in order to stay afloat.

Companies may need to start raising funds for refinancing up to a year before debt comes due in case they need to find new lenders, according to Jochen Schönfelder, a senior partner at Boston Consulting Group in Cologne. He’s already seen firms in Germany cutting back costs and says some are turning to private debt funds if they need cash fast.“Many expect some of the most important sectors in Germany, such as construction and automotive suppliers, to get worse,” Schönfelder said. “The big question is if this will also spill over into plant equipment, machinery, equipment suppliers, and also how private consumption will be affected.”

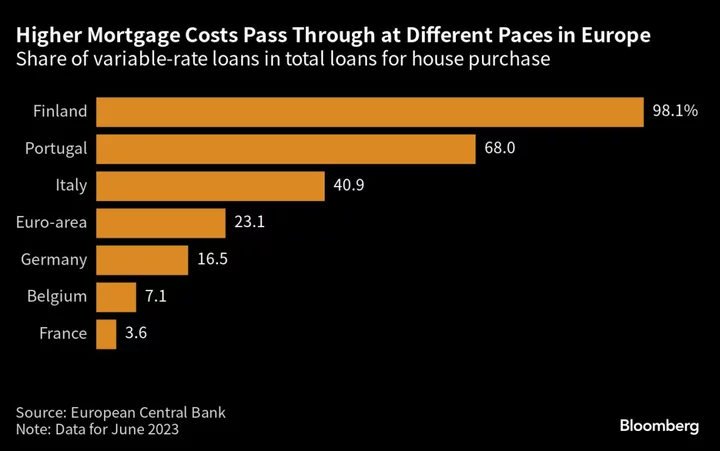

The pain for consumers will mostly be felt through rising mortgage costs and in many countries the rise in interest rates hasn’t yet followed through into monthly payments. The effective interest rate on outstanding home loans in the UK was below 3% as of the end of June, according to the Bank of England, compared with around 6.7% for the average new two-year fixed product, according to data from Moneyfacts. Sweden may serve as a barometer of the pain in store for other countries. Swedish new mortgage holders saw their borrowing costs as a proportion of income double to 10% in 2022, the highest level in at least a decade, according to the country’s Finansinspektionen. That’s caused property prices to plummet, triggering a raft of insolvencies and requests for debt waivers among builders.Another potential pressure point for the continent is the fact that periphery economies like Italy and Portugal have a higher proportion of outstanding floating-rate mortgages. This “remains one of the main risks for a monetary policy hard landing where the weakest economies suffer most,” analysts at Bank of America including Claudio Irigoyen wrote in a recent note to clients.

The higher interest pain is already starting to weigh on state finances. Globally, sovereigns rated by Fitch Ratings face around $2.3 trillion in interest in 2023, representing an increase of nearly 50% for developed markets since 2020. For countries like the UK, where a quarter of government debt is linked to inflation, the burden is higher still. Last month was the most expensive for interest costs of any July on record, according to the latest public finances data.

The burden on governments is already trickling down to councils and sub-national public authorities. Many councils in the UK have been deferring long-term borrowing programs in the hope that rates will decline. “Our advice is basically to sit on your hands and not to borrow long-term this year until inflation, the Bank Rate and gilt yields start to come down,” said David Whelan, a managing director at Link Group, which advises UK local authorities. The problem is that they may be waiting a long time. Earlier this year a string of bank failures led many to forecast that a deeper credit crunch and recession would lead to a deep rate cuts by the end of 2023. But economies proved to be more resilient than expected, making it likely that interest rates will plateau. European Central Bank President Christine Lagarde avoided giving a clear signal of intent for monetary policy in an interview with Bloomberg on Friday. Federal Reserve Chair Jerome Powell has signalled that US borrowing costs will stay high and could even rise further. “The duration of time that we stay in this higher cost of capital, restrictive monetary policy environment is much more important for borrowers” than where interest rates eventually end up, said Amanda Lynam, Head of Macro Credit Research at BlackRock Inc.--With assistance from Jana Randow.