(This story was originally published on March 29. Bank of Japan policymakers meet today, with investors speculating that they will loosen their tight grip on interest rates.)

Read this story in Japanese: 3兆ドルの日銀黒田レガシーが逆回転の恐れ、世界の金融市場に衝撃も

Bank of Japan Governor Haruhiko Kuroda changed the course of global markets when he unleashed a $3.4 trillion firehose of Japanese cash on the investment world. Now Kazuo Ueda is likely to dismantle his legacy, setting the stage for a flow reversal that risks sending shockwaves through the global economy.

Just over a week before a momentous leadership change at the BOJ, investors are gearing up for the seemingly inevitable end to a decade of ultra-low interest rates that punished domestic savers and sent a wall of money overseas. The exodus accelerated after Kuroda moved to suppress bond yields in 2016, culminating in a mountain of offshore investments worth more than two-thirds Japan’s economy.

All this risks unraveling under the new governor Ueda, who may have little choice but to end the world’s boldest easy-money experiment just as rising interest rates elsewhere are already jolting the international banking sector and threatening financial stability. The stakes are enormous: Japanese investors are the biggest foreign holders of US government bonds and own everything from Brazilian debt to European power stations to bundles of risky loans stateside.

An increase in Japan’s borrowing costs threatens to amplify the swings in global bond markets, which are being rocked by the Federal Reserve’s year-long campaign to combat inflation and the new danger of a credit crunch. Against this backdrop, tighter monetary policy by the BOJ is likely to intensify scrutiny of its country’s lenders in the wake of recent bank turmoil in the US and Europe.

A change in policy in Japan is “an additional force that is not being appreciated” and “all G-3 economies in one way or the other will be reducing their balance sheets and tightening policy” when it happens, said Jean Boivin, head of the BlackRock Investment Institute and former Deputy Governor of the Bank of Canada. “When you control a price and loosen the grip, it can be challenging and messy. We think it’s a big deal what happens next.”

The flow reversal is already underway. Japanese investors sold a record amount of overseas debt last year as local yields rose on speculation that the BOJ would normalize policy.

Kuroda added fuel to the fire last December when he relaxed the central bank’s grip on yields by a fraction. In just hours, Japanese government bonds plunged and the yen skyrocketed, jolting everything from Treasuries to the Australian dollar.

“You’ve already seen the start of that money being repatriated back to Japan,” said Jeffrey Atherton, portfolio manager at Man GLG, part of Man Group, the world’s biggest publicly traded hedge fund. “It would be logical for them to bring the money home and not to take the foreign exchange risk,” said Atherton, who runs the Japan CoreAlpha Equity Fund that’s beaten about 94% of its peers in the past year.

Coming Home

Bets for a shift in BOJ policy have eased in recent days as the upheaval in the banking sector raises the prospect that policy makers may prioritize financial stability. Investor scrutiny of Japanese lenders’ balance sheets has grown, on concern they may echo some of the stresses that have floored several regional US banks.

But market participants expect chatter on BOJ tweaks to resume when tensions dissipate.

Why Japanese Banks Are Well Placed to Withstand Banking Crisis

Ueda, the first ever academic to captain the BOJ, is largely expected to speed up the pace of policy tightening sometime later this year. Part of that may include further loosening the central bank’s control on yields and unwinding a titanic bond-buying program designed to suppress borrowing costs and boost Japan’s moribund economy.

The BOJ has bought 465 trillion yen ($3.55 trillion) of Japanese government bonds since Kuroda implemented quantitative easing a decade ago, according to central bank data, depressing yields and fueling unprecedented distortions in the sovereign debt market. As a result, local funds sold 206 trillion yen of the securities during the period to seek better returns elsewhere.

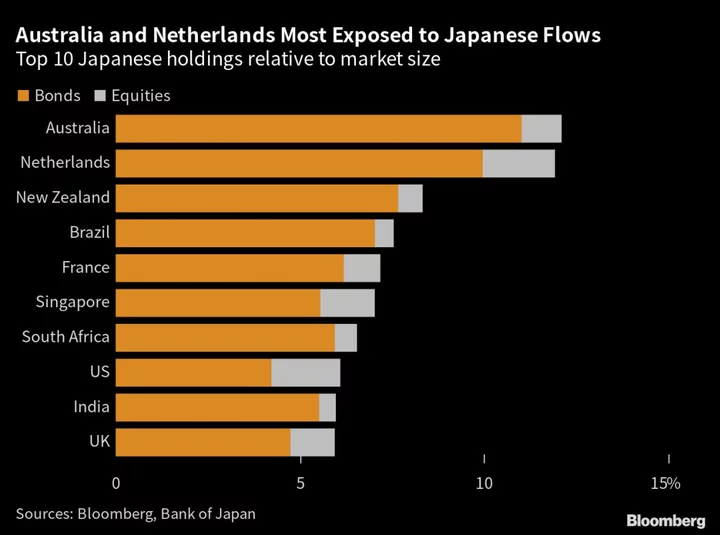

The shift was so seismic that Japanese investors became the biggest holders of Treasuries outside the US as well as owners of about 10% of Australian debt and Dutch bonds. They also own 8% of New Zealand’s securities and 7% of Brazil’s debt, calculations by Bloomberg show.

The reach extends to stocks, with Japanese investors having splashed out 54.1 trillion yen on global shares since April 2013. Their holdings of equities are equivalent to between 1% and 2% of the stock markets in the US, Netherlands, Singapore and the UK.

Japan’s ultra-low rates were a big reason the yen tumbled to a 32-year low last year, and it has been a top option for income-seeking carry traders to fund purchases of currencies ranging from Brazil’s real to the Indonesian rupiah.

“Almost definitely it contributed to a significant decline of the yen, a massive dysfunctioning of the Japanese bond market,” former UK government minister and Goldman Sachs Group Inc. chief economist Jim O’Neill said of Kuroda’s policies. “Much of what happened in Kuroda’s time will partially or fully reverse” should his successor pursue policy normalization, although the banking crisis may cause authorities to proceed more cautiously, he added.

The currency has pulled back from last year’s lows, helped by a view that normalization is inevitable.

Add to that equation last year’s historic global bond losses, and Japanese investors have even more reason to flock home, according to Akira Takei, a 36-year market veteran and money manager at Asset Management One Co.

“Japanese debt investors have had bad experiences outside the country in the past year because a substantial jump in yields forced them to cut losses, so many of them even don’t want to see foreign bonds,” said Tokyo-based Takei, whose firm oversees $460 billion. “They are now thinking that not all funds have to be invested abroad but can be invested locally.”

The incoming president of Dai-ichi Life Holdings Inc., one of Japan’s largest institutional investors, confirmed it was shifting more money to domestic bonds from foreign securities, after aggressive US rate hikes made it costly to hedge against currency risks.

To be sure, few are prepared to go all out in betting Ueda will rock the boat once he gets into office.

A recent Bloomberg survey showed 41% of BOJ watchers see a tightening step taking place in June, up from 26% in February, while former Japan Vice Finance Minister Eisuke Sakakibara said the BOJ may raise rates by October.

A summary of opinions from the BOJ’s March 9-10 meeting showed the central bank remains cautious about executing a policy pivot before achieving its inflation target. And that was even after Japan’s inflation accelerated beyond 4% to set a fresh four-decade high.

The next central bank meeting, Ueda’s first, is scheduled to take place April 27-28.

Richard Clarida, who served as Vice Chairman at the Federal Reserve from 2018 to 2022, arguably has more insight than most after having known “straight shooter” Kuroda for years and weighed Japan’s impact on US and global monetary policy.

“Markets expect pretty early under Ueda that yield-curve control is dismantled,” said Clarida, who is now global economic advisor at Pacific Investment Management Co. From here Ueda “may want to go in the direction to shrink the balance sheet or reinvest the redemptions, but that is not one for day one,” he said, adding Japan’s tightening would be a “historic moment” for markets though it may not be a “driver of global bonds.”

Gradual Shift

Some other market watchers have more modest expectations of what will happen once the BOJ rolls back its stimulus program.

Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Ltd., sees the US-Japan rate gap persisting to a degree as the Fed is unlikely to deliver large rate cuts if inflation remains high and the BOJ isn’t expected to raise rates substantially in the near term.

“It’s important to assess any tweaks and outlooks of the BOJ’s whole monetary policy package when thinking about their implication on the cross-border fund flows,” she said.

Ryosuke Oshima, deputy general manager of product promotion group at Mitsubishi UFJ Kokusai Asset Management Co. in Tokyo, is eyeing yield levels as a potential trigger for a shift in flows.

“There might be some appetite for bond funds when the rates move higher, like 1% for the 10-year yield,” he said. “But looking at the data, it is unlikely they reverse all their investment back home suddenly.”

For others like 36-year markets veteran Rajeev De Mello, it’s likely only a matter of time before Ueda has to act and the consequences may have global repercussions.

“I fully agree with the consensus that the BOJ will tighten — they’ll want to end this policy as soon as possible,” said De Mello, a money manager at GAMA Asset Management in Geneva. “It comes down to central bank credibility, it comes down to inflation conditions being increasingly fulfilled now — normalization will come to Japan.”

((This story was originally published on March 29.Bank of Japan policymakers meet today, with investors speculating thatthey will loosen their tight grip on interest rates.))

Author: Ruth Carson, Masaki Kondo and Michael Mackenzie